16 November 2022

Emilie Paquet, FSA, Head of Strategic Initiatives and Innovation, Multi-Asset Solutions Team

Jeffrey Kan, CFA, Senior Portfolio Manager, Multi-Asset Solutions Team Asia

Paul Kalogirou, Managing Director, Client Portfolio Manager, Multi-Asset Solutions Team, Asia

Where to find income in today’s tumultuous investment world? This is one challenge often faced by investors of this generation. In Asia, major cities have seen home prices rise by 19% on average in the last five years. Meanwhile, the average wage growth in Asia has fallen short, rising only 3% on average over the same period.1 Higher inflation outpacing income growth is just one of the many challenges that investors in the region are facing. The easy days of predictability are over. In recent years, there has been no shortage of surprises including stock market volatility and interest rate rises. How can regular investors find stable and sustainable income to meet their long-term objectives, particularly in today’s inflationary and unpredictable investment environment?

What’s more, how can investors use their income (from active employment or savings) to cover future expenses and will it last beyond retirement? Finally, where can individuals find diversified sources of higher income? We discuss how investors in challenging and uncertain times can achieve relatively more reliable and potentially higher income throughout their lifetime.

There has been no shortage of market crises in the last decade. In fact, the twist and turns in economic cycles have provided a valuable lesson for income-seeking investors: do not limit yourself to one asset class or rely on capital gains to harvest income — multi-asset investing can create diversification benefits and potentially higher income in a volatile market.

Historically, traditional assets dominated in the past decades and provided sources of income by paying out from capital gains. Asian and US equities, for instance, gained 66% and 43% respectively from 2002 to 2008 as income-seeking investors enjoyed the income stream profited from an economic boom.2 US Treasuries (10-yield rose to average 4%) also provided another stable source of income during the same period. However, the tides have reversed since 2018 and non-traditional assets are beginning to make headways. For example, commodities have risen by 33% in the last four years, whereas global REITs have risen by 4% in the last two years.3

Who will be the winners and losers of income in the next decade? And how can income-seeking investors opportunistically position a portfolio going forward without taking on unwanted risk? Where can they find stable sources of income from natural yields (the cashflow generated from investments)? Let us illustrate how to position income-focused portfolios in today’s world.

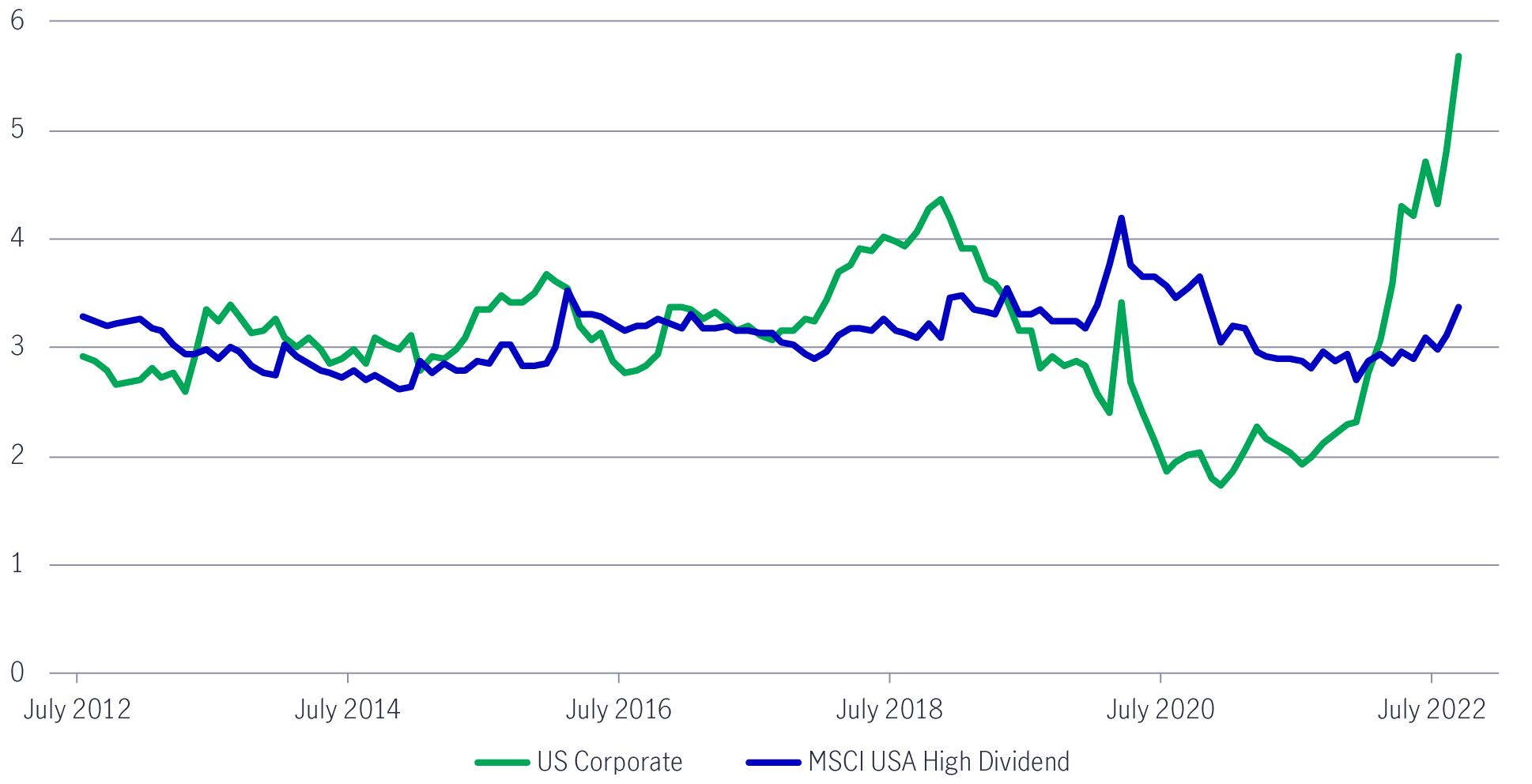

A flexible investment approach that can timely shift between asset allocations during market volatility can help stabilize a portfolio’s income stream. We compared Investment Grade yields vs the MSCI USA High Dividend Yield index4, and found both asset classes provided comparable income (yields) from 2012 to 2018. (Chart 1)

The difference between the two asset classes has widened in recent years. From 2019 to 2021, dividend-paying equities have been paying more income than investment grade bonds, while also offering the opportunity for earnings growth. However, since 2022 investment grade yields have moved significantly higher than their dividend-paying equities and are generally considered lower risk. This highlights why, as the investing environment changes, a more agile investment approach might benefit from the flexibility of shifting between two asset classes.

Chart 1: Yield (%) comparison between US investment grade bonds and dividend-paying equities

Source: Bloomberg as of 30 September 2022. The Bloomberg US Corporate Bond Index measures the investment grade, fixed-rate, taxable corporate bond market and USD denominated securities publicly issued by US and non-US industrial, utility and financial issuers. The MSCI USA High Dividend Yield measures securities with dividend yield of at least 30% higher than the respective parent MSCI equity index and a non-negative 5Y Dividends per share (DPS) growth rate.

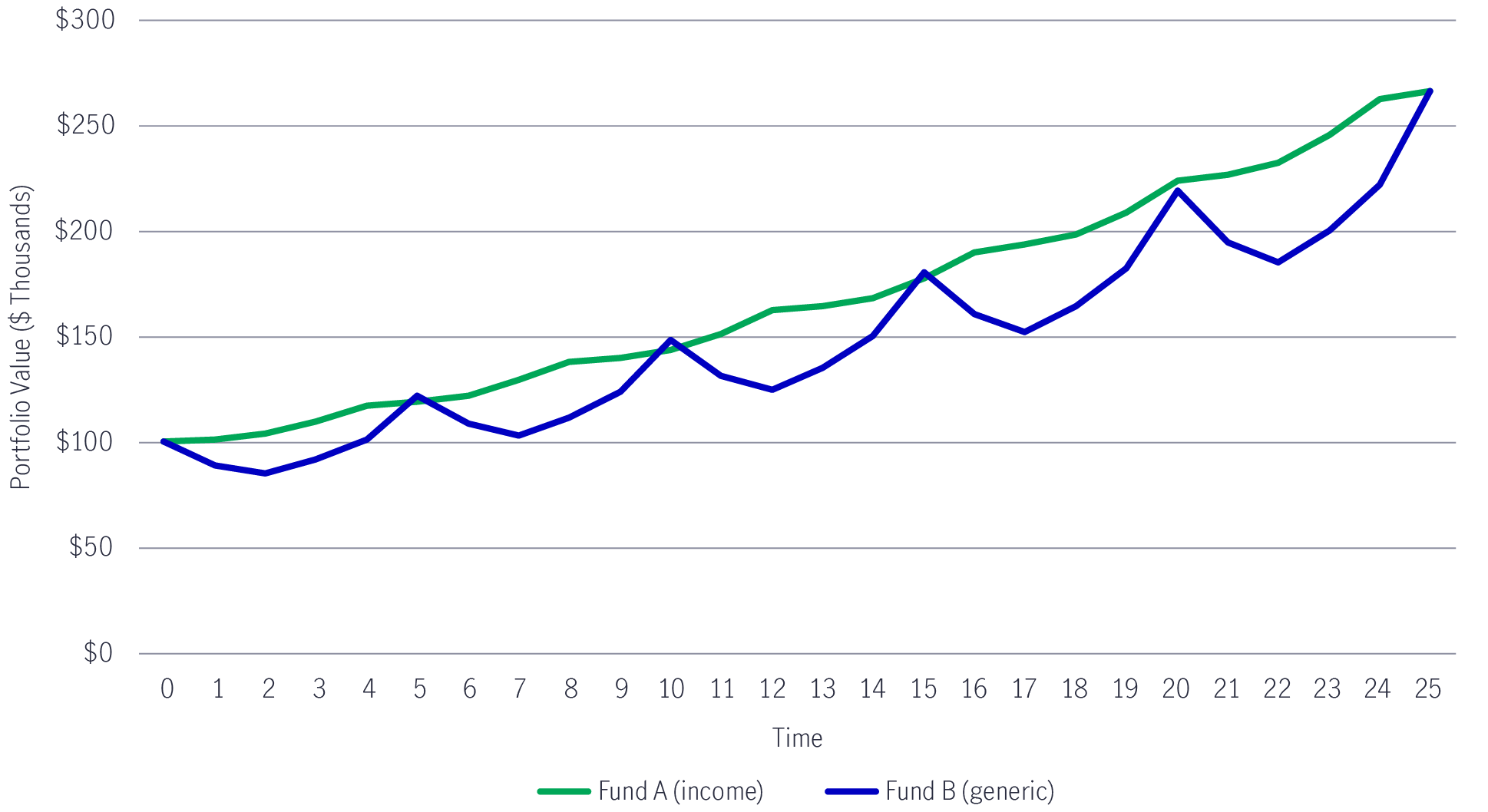

In this scenario, we show why it’s critical to determine the frequency and magnitude of future income needs early on. Let’s take Mike (40 years old, average income earner) for example. He is in his accumulation (asset growth) phase. He is employed and receives active income from working, but he also saves for forthcoming family expenses and retirement with a longer-term horizon. During this phase, Mike begins contributing to his regular savings plan at Year 1, focusing on growing and accumulating his assets. He expects a 4% average return on his savings capital for the next 25 years.

Mike has two funds to choose from: Fund A (a multi-asset fund with an income focus)5 and Fund B (generic multi-asset fund)6. Both funds can invest in a diverse mix of equities, fixed income and equity-related securities. The main difference is that Fund A has an income-oriented goal of generating high, stable income throughout the investment period, whereas Fund B is a generic fund with no such goal. If Mike does not make any withdrawals from this capital pool, both funds (A and B) will provide a 4% annualized return over the 25-year period. (Chart 2)

Chart 2: An income-focused fund (A) can provide a more stable path of returns than a generic fund (B)

Portfolio Value ($ thousands)

The above asset allocation is for illustrative purpose only and does not represent the actual investment.

However, the path of return with Fund A (income-oriented fund) will be less volatile during market ups and downs. If Mike does withdraw (to satisfy his income needs) during the accumulation phase, his capital pool might fluctuate more (and might suffer a capital loss in the end) during the ups and downs if generic Fund B is held instead of income Fund A. For example, Mike begins with $100,000 in his portfolio at Year 0. At Year 2, there is a market downturn and the value of Mike’s portfolio either rises to $104,038 with income Fund A or declines to $84,550 with generic Fund B. Similarly, at Year 23, Mike is two years shy of retirement, his portfolio value is either $245,230 with income fund A or $199,850 with generic fund B, depending on which fund he chose at the beginning.

In this scenario, even though Fund B (generic) enjoyed some periods of market upturns (Years 5, 10, 15, 20 and 25), too many negative returns early on, coupled with constant withdrawal amounts will simply deplete Mike’s accumulated capital pool. In fact, Mike would not have enough capital to withdraw during market downturns (Years 2, 7, 12, 17 and 22), when he is most likely to need income. We believe investors should diversify into multi-asset income investments to avoid a negative sequence of returns, which could seriously impede the individual’s ability to realize stable income while making his or her capital last until the end.

In the last decade and beyond, traditional sources of income have run its course and investors need to find and diversify into alternative and natural-yielding sources of income.

We believe the portfolio construction process begins with a specific objective: a high level of consistent, stable income, without jeopardizing the volatility of the overall strategy, and minimizing investor exposure to outsize risk. For sustainable long-term income, a multi-asset portfolio can be customized to achieve higher natural yields (the cash generated from invested income sources) that are closer to or even equal to a portfolio’s overall payout target, whilst minimising the reliance on capital appreciation of the underlying growth assets within the portfolio.

A portfolio with reasonably high natural yield in relation to its overall payout, can help an investor in generating a decent income from the underlying investments (rather than selling your investments to fund your spending). This could be dividends from equities, or the coupons paid on bonds. Natural yields can be an attractive investment tool, particularly during the decumulation phase whilst in retirement for example (when increased withdrawals are required). If the underlying natural yield of a portfolio is sustainable, that helps investors meet their monetary goals, there is less incentive to sell those assets. Relying on natural-yielding income, rather than a reliance on the asset appreciating in value — which may be challenged in a negative market environment, gives your capital a longer-term investment horizon to grow, and possibly ride through any downturns; thus, maximizing the chance of the capital lasting longer.

Moreover, a multi-asset portfolio can give investors access to a wider range of income-generating assets, as well as greater depth and diversification within asset classes.

Here are the diverse sources of income that could be found in a multi-asset portfolio:

1) Higher-yielding fixed income and equities (investment grade, high yield, and emerging market bonds and global equities)

2) Non-traditional/alternative income (preferred securities, REITS, option-writing)

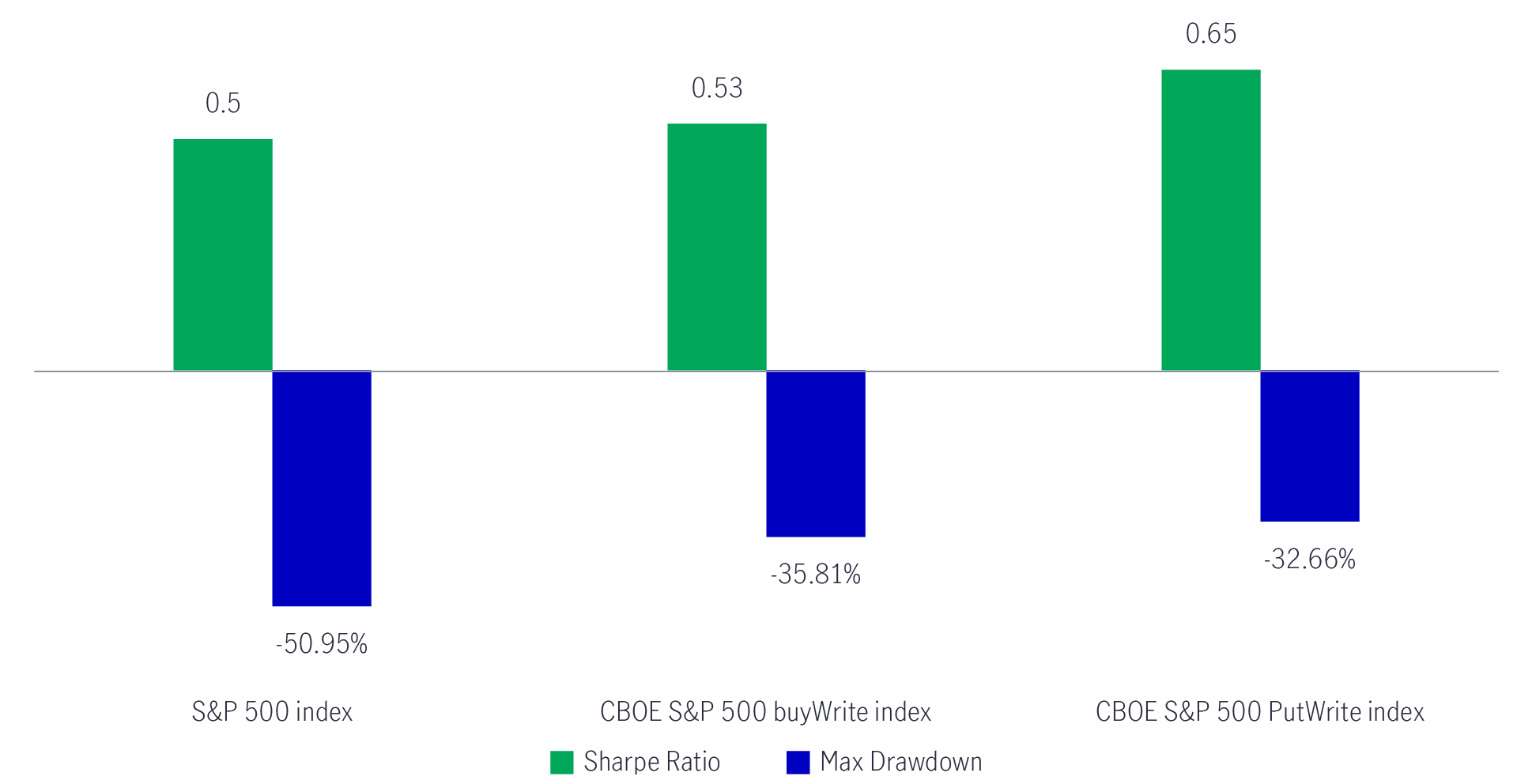

Chart 3: Options writing can potentially provide income and limit maximum drawdowns (index returns from July 1986 to May 2019)

Source: Bloomberg, CBOE, S&P. Data from July 1986 to May 2019. Sharpe ratio measures the risk-adjusted return of index by calculating the average investment return, minus the risk-free rate, divided by the standard deviation. Maximum drawdown measures the largest decline in the value of the index from peak to trough. It is not possible to invest directly into an index. No investment strategy or risk management technique or guarantee returns or eliminate risk in any market environment. It is not possible to invest in indices.

Therefore, in a highly volatile and uncertain environment, multi-asset investing provides investors with a flexibility to access income tools that could provide downside protection – which would not only better preserve capital for investors in a particular year, but also help investors avoid a negative sequence of returns. This would greatly help an individual’s ability to realize stable income while making their capital last longer. Furthermore, an investor could re-invest cashflows achieved from income generated by a multi-asset income portfolio. In the next section, we’ll highlight the challenges that income seekers could face in the next cycle, and our outlook towards asset classes that provide the highest potential for income investors.

Global risk markets are likely to face a few headwinds, in the short term at least: inflation is likely to remain elevated for some time, a hawkish Fed profile, rising rates and a stagflationary macro backdrop (elevated inflation, slowing growth). Despite these exogenous shocks, growth in the Asia-Pacific region is still holding up relatively well, having benefited from the reopening of global supply chains and favourable demographics and consumption trends. More than half of the region’s economies saw their annual inflation ease in the third quarter.8 Should this trend continue, it could support a shallow and shorter tightening cycle in Asia relative to other regions.

Under a challenging period for risk markets, we believe multi-asset investing with the agility to shift allocations across asset classes and geographies can still help to generate income within a market downturn.

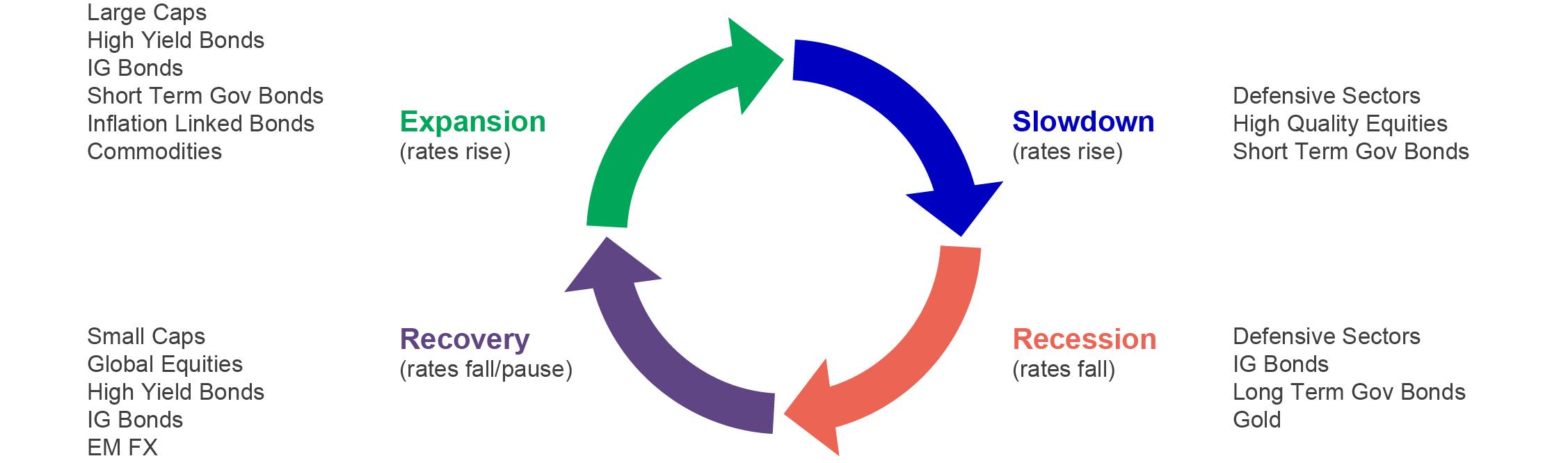

As we approach the final innings of the economic slowdown, we see opportunities in select government bonds, as well as high-quality equities (stocks that offer the prospect of capital appreciation in addition to dividends). (Chart 4) These are stable businesses with solid balance sheets and companies which show ongoing earnings resilience, potentially offering relative protection if earnings come under pressure. Select commodity-related economies could also benefit from tight supply dynamics. Where appropriate, multi-asset income-oriented portfolios could use option-writing strategies to harvest option premiums, which can enhance portfolio yields.

Chart 4: Asset allocation during the stages of the economic cycle

Interest rate hikes are expected to gradually peak near the end of an economic slowdown, while rates tend to decline during a recession as loan demand slows and monetary policy eases. We believe the outlook for these asset classes are well-positioned for the current market cycle:

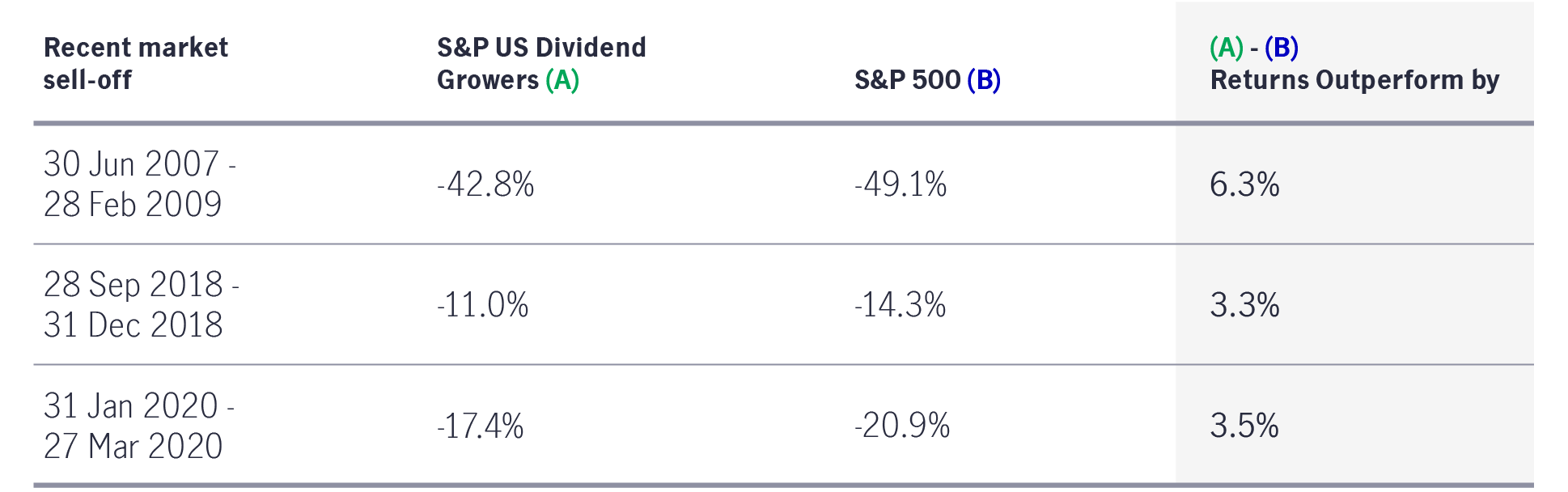

Chart 5: Dividend growers have outperformed during market sell-offs and rising rates

Why invest in alternative investments now

A new macroeconomic regime strengthens the case for alternative investment allocations that go beyond the 60/40 stock-bond investor portfolios.

Banking stress has created a yield premium for preferred securities

The banking crisis weighed heavily on preferred securities earlier this year but has now created a potential opportunity relative to riskier areas of the fixed-income market.

Global Macro Outlook Q3 2023: The long and winding road

At the time of writing, only the eurozone and New Zealand have slipped into recession (as defined by two consecutive quarters of negative growth). But don’t pop the champagne just yet: We see this as a case of recession postponed rather than canceled. Read more.

Solutions for navigating market volatility amid U.S. tariff changes

Recent changes in U.S. tariffs have introduced new dynamics to the global market landscape, presenting both challenges and opportunities for investors. Understanding these developments is essential for making informed investment decisions. Marc Franklin, our Deputy Head of Multi-Asset Solutions, Asia, and Senior Portfolio Manager provided his view.

Quick thoughts on US reciprocal tariffs

The US President Donald Trump announced reciprocal tariff details on 2 April, 2025, which has introduced volatility to the financial markets. Alex Grassino, Global Chief Economist, along with the Multi-Asset Solutions Team (MAST), Macroeconomic Strategy Team, share their latest views.

Takeaways from China’s NPC Meeting & upcoming drivers for Greater China equity market

In addition to the recent breakthroughs in AI and humanoid robot development, we observe other positive catalysts that further support the region’s market.

Source: Bloomberg as of 30 September 2022. The S&P U.S. Dividend Growers Index is designed to measure the performance of U.S. companies that have followed a policy of consistently increasing dividends every year for at least 10 consecutive years. The index excludes the top 25% highest-yielding eligible companies from the index. It is not possible to invest in indices.

Should a portfolio also deploy dynamic asset allocation drivers, a portfolio’s income can be harvested and managed from diversified sources. The reason why multi-asset income investing is so important for income seekers is because each sector of the economy or asset class can perform differently from another at any given time in a market cycle. We can also find compelling investment opportunities down in the capital structure that offer a better natural-yielding income and return profile, focus on risk-adjusted returns and find opportunities that are less sensitive to rising interest rates, while moving between different income segments during fluctuating economic cycles.

In this decade, there is an increasing and urgent demand for sophisticated “outcome based” investment solutions for investors. These solutions, which essentially have their core investment process customized to a specific outcome, are becoming more advanced in their design and construction. Investment managers with a more agile approach to asset allocation can fine-tune these solutions more precisely to investor needs. Specifically, the demand for multi-asset income investing is rapidly gaining traction, thanks to an aging population and its insatiable demand for income. Research shows that by 2050, the elderly population in Asia will account for 63% of the world’s aged population10. Asia must develop its own retirement income solutions to cater for its diverse demographics. The same study indicates Asian middle-income workers are saving for retirement but need focused solutions that provide stable income streams as persistent inflation erodes their self-made earnings. Market volatility from an uncertain geopolitical environment, as well as regulatory requirements/tax considerations and compliance of ESG (environmental, social, and governance) standards, could also impact one’s investment decisions. While these factors present challenges, they can create fresh income opportunities for today’s multi-asset investors.

1 Bloomberg for period 30 September 2017 to 30 September 2022. Based on data available for nationwide residential property prices for Hong Kong, Singapore, Japan, China, India, Indonesia, Korea, and Thailand. Based on data available for annual wage growth for Hong Kong, Singapore, India, Indonesia, and Thailand, total remuneration cash or in kind for Japan and disposable income per capita for China for 30 September 2017 to 30 September 2022. Based on data available for annual wage for Korea for 30 September 2021 to 30 September 2022.

2 Bloomberg for period 30 September 2002 to 30 September 2008. Based on data for MSCI AC Asia Pacific index and Dow Jones Industrial Average index.

3 Bloomberg data for Commodities is measured by S&P GSCI commodity index for 30 October 2018 to 30 September 2022. Global REIT is measured by FTSE EPRA Nareit Global REITs Index for 30 October 2020 to 30 September 2022.

4 A proxy for a diversified mix of relatively reasonable quality, dividend-paying equities. It is not possible to invest in indices.

5 Fund A strategy aims to generate high, stable income through multiple income sources. It is a diversified portfolio of equity, equity-related, fixed income and fixed income-related securities of companies and/or governments globally.

6 Fund B strategy does not specify an income objective. It is a diversified portfolio of equity, equity-related, fixed income and fixed income-related securities of companies and/or governments globally.

7 Selling options (the portfolio) give investors (the buyer) the right - but not the obligation - to buy (in the case of calls) or sell (in the case of puts) an underlying instrument at the contractual strike price. Investors pay a premium for the right to exercise that option at the strike price.

8 Manulife Investment Management, Global Macro Outlook Q4 2022: A difficult climb ahead, September 2022.

9 MSCI, based on index factsheets of MSCI USA Consumer Staples Index (USD), MSCI USA Health Care Index (USD), MSCI USA Utilities Index (USD) as of 30 September 2022.

10 Manulife Investment Management, Diverse Asia whitepaper, November 2022.